Tokenized Treasuries vs exchange Earn: where should your $10K sit in 2026?

Tokenized US Treasuries just crossed $15B and now compete with exchange Earn. Government-grade ~3.35% vs 7%+ on a platform — same dollar, very different risk. Here's how to choose, safety-first.

In June 2026, tokenized US Treasuries quietly crossed $15 billion in assets. BlackRock's tokenized fund alone (BUIDL) passed $5 billion. For the first time, a boring government bond — wrapped as a crypto token — competes directly with the exchange "Earn" products this site tracks. So if you have, say, $10,000 in stablecoins sitting idle, you now have a real choice: park it in a tokenized Treasury at around 3.35%, or chase 7%+ on an exchange. This article is about making that choice with your eyes open.

What a tokenized Treasury actually is

A US Treasury is debt issued by the American government — the closest thing finance has to a "risk-free" asset. It pays a yield (recently ~4–5% on short maturities) and is backed by the full faith and credit of the United States.

"Tokenized" means a regulated issuer buys real Treasury bills, holds them, and issues a blockchain token backed 1:1 by that holding. You hold the token; the token earns the Treasury's yield, paid on-chain. The big names already do this: BlackRock (BUIDL), Franklin Templeton (BENJI), Ondo (OUSG / USDY), plus JPMorgan's on-chain money-market efforts. Per RWA.xyz, the category sat near $14.8B with a ~3.35% 7-day yield in early June 2026.

The pitch is simple: government-grade yield, on-chain, around the clock, without a traditional bank in the middle.

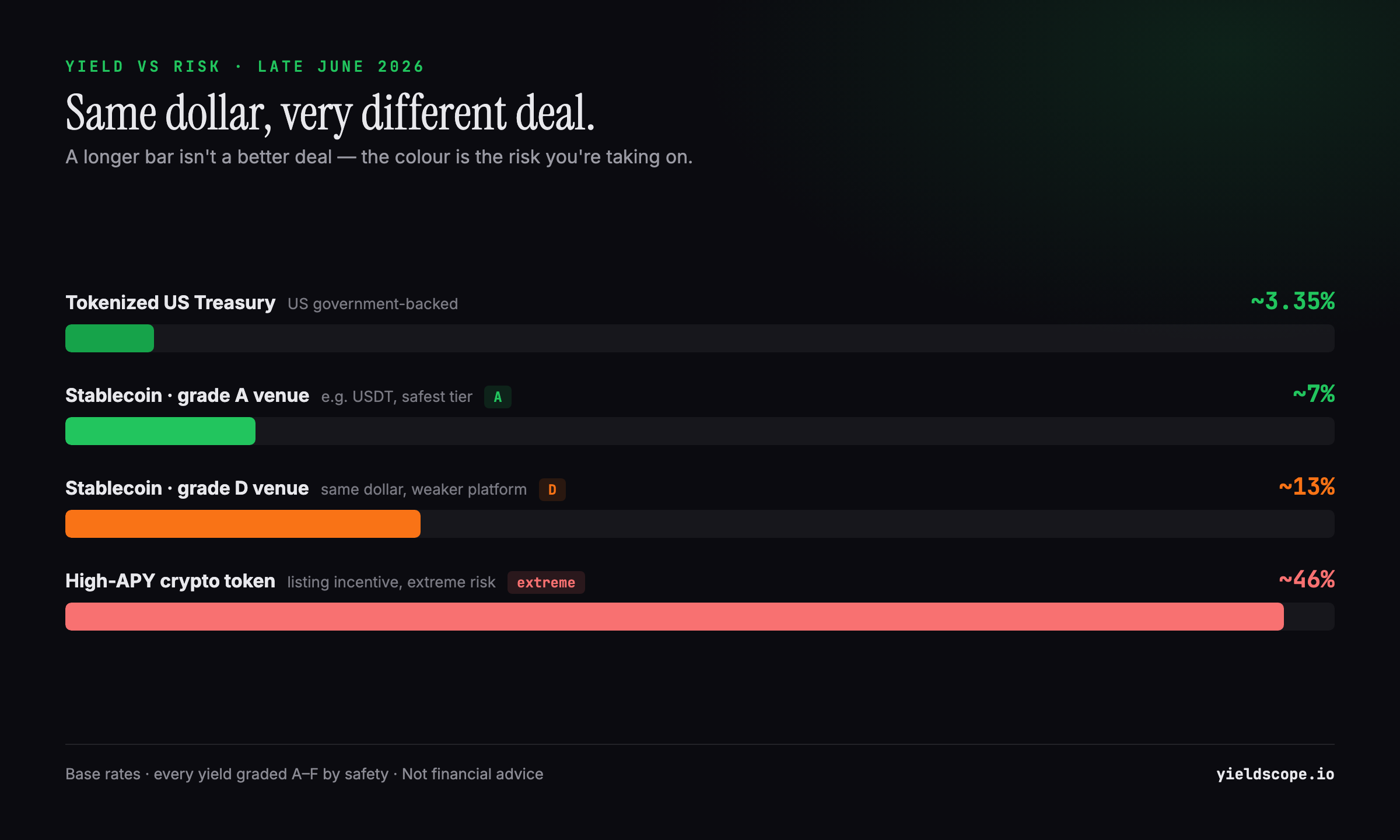

The numbers, side by side

Here is the honest comparison as of late June 2026:

| Option | Typical yield | What backs it |

|---|---|---|

| Tokenized Treasury | ~3.35% | Short-dated US government debt |

| Stablecoin on a top-graded exchange | ~7% (e.g. USDT on a grade-A venue) | The platform's lending / market-making |

| Stablecoin on a weaker venue | 12–13%+ | Same, but lower safety grade |

| High-APY crypto tokens | 30–46%+ | Listing incentives, extreme risk |

On rate alone, the exchange wins — 7% beats 3.35%, and the flashy venues advertise double that. But "rate alone" is exactly the trap. The right question is not which number is bigger, it's what am I being paid to take on?

Same dollar, very different risk

This is where the comparison gets interesting, and where our A–F safety grades exist.

Tokenized Treasury risk. The underlying asset — US government debt — is about as safe as finance gets. But the wrapper adds risk you don't have with a paper bond: the smart contract could have a bug, the issuer could mismanage redemptions, and access depends on the token staying liquid and redeemable. The credit risk is tiny; the plumbing risk is real but generally well-audited for the large issuers.

Exchange Earn risk. When you earn 7% on USDT, the dollar itself isn't the risk — the platform is. The exchange puts your deposit to work (typically lending plus market-making) and shares the return. If the platform becomes insolvent, gets hacked, or freezes withdrawals, your "safe" stablecoin can be stuck or lost. That's why a grade-A venue paying 7% and a grade-D venue paying 13% are not the same deal at all — the extra 6% is the market pricing in extra risk.

A useful way to read it: a tokenized Treasury moves most of your risk to the smart-contract/issuer layer; an exchange Earn product concentrates it on the platform's solvency. Neither is "risk-free" — they just fail in different ways.

So where should $10K go?

There is no single right answer — it depends on what you're optimizing for.

If your priority is capital preservation (you'd be upset to lose any of it): a tokenized Treasury from a major, audited issuer is hard to beat. ~3.35% backed by US government debt is a genuinely conservative home for idle dollars — closer to a money-market fund than to crypto speculation.

If you want more yield and accept platform risk: a stablecoin Earn product on a high-grade exchange can pay roughly double, and for many people that trade-off is reasonable — if they pick the venue on safety, not on the headline rate. This is the entire reason we grade every platform A–F.

If you're chasing 30–46% on a volatile token: understand that you're no longer comparing with Treasuries at all. Those rates are listing incentives on extreme-risk assets, and the principal can move far more than the yield. We flag them, but they belong in a different mental bucket entirely.

A sensible split many people land on: a core of conservative yield (tokenized Treasuries or a grade-A stablecoin product) and a small, clearly-labelled satellite for higher-risk bets — never the reverse.

A safety-first way to decide

Whatever you choose, run the same three checks before depositing:

- What's the real backing? Government debt, platform lending, or token incentives? That tells you the failure mode.

- What's the grade? On YieldScope every exchange carries an A–F score across regulation, proof of reserves, withdrawal flexibility, insurance fund, and incident history. Use it.

- Is the extra yield worth the extra risk? Going from 3.35% to 7% on a grade-A venue is a defensible step. Going from 7% to 13% by dropping to grade D usually isn't — you're being paid a little to take on a lot.

You can compare live stablecoin rates with their safety grades on our stablecoins board, and read how the grading works on the transparency page.

Bottom line

Tokenized Treasuries crossing $15B is a real shift: for the first time, "boring" government yield is available on-chain and competes head-to-head with exchange Earn. It won't pay the most — but it changes the baseline. The smart move isn't to pick the biggest number; it's to decide how much risk you actually want, then take the best rate available at that level of safety. That's the whole job this site is built to make easy.

Disclosure: YieldScope is an information service, not investment advice. Rates and figures are snapshots and change; verify before acting.

Educational content, not financial or legal advice. Sources are linked in the text.